My life has been to seek the Absolute Truth of God; to help others find the real purpose of their lives... Attempt to make this or where ever I am; better for my having been there! Amen!

President Nixon walks with Saudi King Faisal in Saudi Arabia in June 1974.

Failure was not an option.

It

was July 1974. A steady predawn drizzle had given way to overcast skies

when William Simon, newly appointed U.S. Treasury secretary, and his

deputy, Gerry Parsky, stepped onto an 8 a.m. flight from Andrews Air

Force Base. On board, the mood was tense. That year, the oil crisis had

hit home. An embargo by OPEC’s Arab nations—payback for U.S. military

aid to the Israelis during the Yom Kippur War—quadrupled oil prices.

Inflation soared, the stock market crashed, and the U.S. economy was in a

tailspin.

Officially, Simon’s two-week trip was billed as a tour

of economic diplomacy across Europe and the Middle East, full of the

customary meet-and-greets and evening banquets. But the real mission,

kept in strict confidence within President Richard Nixon’s inner circle,

would take place during a four-day layover in the coastal city of

Jeddah, Saudi Arabia.

The goal: neutralize crude oil as an

economic weapon and find a way to persuade a hostile kingdom to finance

America’s widening deficit with its newfound petrodollar wealth. And

according to Parsky, Nixon made clear there was simply no coming back

empty-handed. Failure would not only jeopardize America’s financial

health but could also give the Soviet Union an opening to make further

inroads into the Arab world.

It “wasn’t a question of whether it

could be done or it couldn’t be done,” said Parsky, 73, one of the few

officials with Simon during the Saudi talks.

Treasury

Secretary William Simon, left, sits with Nancy Kissinger and Secretary

of State Henry Kissinger as they listen to former President Nixon talk

to his staff prior to leaving the White House for the last time, August

9, 1974.

Source: AP Photo

At

first blush, Simon, who had just done a stint as Nixon’s energy czar,

seemed ill-suited for such delicate diplomacy. Before being tapped by

Nixon, the chain-smoking New Jersey native ran the vaunted Treasuries

desk at Salomon Brothers. To career bureaucrats, the brash Wall Street

bond trader—who once compared himself to Genghis Khan—had a temper and

an outsize ego that was painfully out of step in Washington. Just a week

before setting foot in Saudi Arabia, Simon publicly lambasted the Shah

of Iran, a close regional ally at the time, calling him a “nut.”

But

Simon, better than anyone else, understood the appeal of U.S.

government debt and how to sell the Saudis on the idea that America was

the safest place to park their petrodollars. With that knowledge, the

administration hatched an unprecedented do-or-die plan that would come

to influence just about every aspect of U.S.-Saudi relations over the

next four decades (Simon died in 2000 at the age of 72).

The basic

framework was strikingly simple. The U.S. would buy oil from Saudi

Arabia and provide the kingdom military aid and equipment. In return,

the Saudis would plow billions of their petrodollar revenue back into

Treasuries and finance America’s spending.

It took several

discreet follow-up meetings to iron out all the details, Parsky said.

But at the end of months of negotiations, there remained one small, yet

crucial, catch: King Faisal bin Abdulaziz Al Saud demanded the country’s

Treasury purchases stay “strictly secret,” according to a diplomatic

cable obtained by Bloomberg from the National Archives database. Special Report:Where Next for Saudi Arabia?

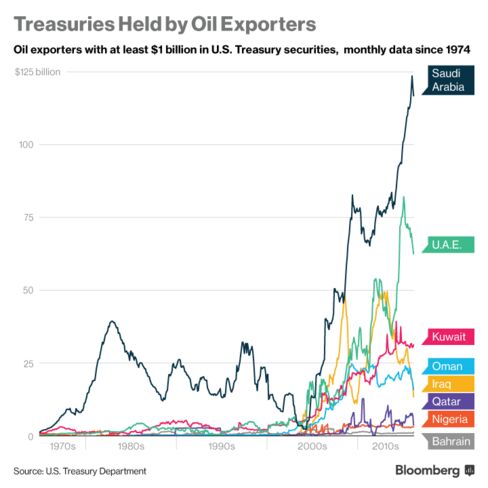

With

a handful of Treasury and Federal Reserve officials, the secret was

kept for more than four decades—until now. In response to a

Freedom-of-Information-Act request submitted by Bloomberg News, the

Treasury broke out Saudi Arabia’s holdings for the first time this month

after “concluding that it was consistent with transparency and the law

to disclose the data,” according to spokeswoman Whitney Smith. The $117

billion trove makes the kingdom one of America’s largest foreign

creditors.

Yet in many ways, the information has raised more

questions than it has answered. A former Treasury official, who

specialized in central bank reserves and asked not to be identified,

says the official figure vastly understates Saudi Arabia’s investments

in U.S. government debt, which may be double or more.

The current

tally represents just 20 percent of its $587 billion of foreign

reserves, well below the two-thirds that central banks typically keep in

dollar assets. Some analysts speculate the kingdom may be masking its

U.S. debt holdings by accumulating Treasuries through offshore financial

centers, which show up in the data of other countries.

Drivers

line up for fuel at a U.S. gas station during the worldwide fuel

shortages caused by the oil embargo imposed by OPEC, circa 1974.

Exactly how much of America’s debt Saudi Arabia actually owns is something that matters more now than ever before.

While

oil’s collapse has deepened concern that Saudi Arabia will need to

liquidate its Treasuries to raise cash, a more troubling worry has also

emerged: the specter of the kingdom using its outsize position in the

world’s most important debt market as a political weapon, much as it did

with oil in the 1970s.

In April, Saudi Arabia warned it would

start selling as much as $750 billion in Treasuries and other assets if

Congress passes a bill allowing the kingdom to be held liable in U.S.

courts for the Sept. 11 terrorist attacks, according to the New York Times.

The threat comes amid a renewed push by presidential candidates and

legislators from both the Democratic and Republican parties to

declassify a 28-page section of a 2004 U.S. government report that is

believed to detail possible Saudi connections to the attacks. The bill,

which passed the Senate on May 17, is now in the House of

Representatives.

Saudi Arabia’s Finance Ministry declined to

comment on the potential selling of Treasuries in response. The Saudi

Arabian Monetary Agency didn’t immediately answer requests for details

on the total size of its U.S. government debt holdings.

“Let’s not

assume they’re bluffing” about threatening to retaliate, said Marc

Chandler, the global head of currency strategy at Brown Brothers

Harriman. “The Saudis are under a lot of pressure. I’d say that we don’t

do ourselves justice if we underestimate our liabilities” to big

holders.

What's the Untold Story of Saudi Arabia's Debt Secret?

President Nixon shakes hands with Saudi King Faisal in June, 1974, in Saudi Arabia.

Photographer: Dirck Halstead/Liaison via AP Photo

Saudi

Arabia, which has long provided free health care, gasoline subsidies,

and routine pay raises to its citizens with its petroleum wealth,

already faces a brutal fiscal crisis.

In the past year alone, the

monetary authority has burned through $111 billion of reserves to plug

its biggest budget deficit in a quarter-century, pay for costly wars to

defeat the Islamic State, and wage proxy campaigns against Iran. Though

oil has stabilized at about $50 a barrel (from less than $30 earlier

this year), it’s still far below the heady years of $100-a-barrel crude.

Saudi

Arabia’s situation has become so acute the kingdom is now selling a

piece of its crown jewel—state oil company Saudi Aramco.

What’s

more, the commitment to the decades-old policy of “interdependence”

between the U.S. and Saudi Arabia, which arose from Simon’s debt deal

and ultimately bound together two nations that share few common values,

is showing signs of fraying. America has taken tentative steps toward a

rapprochement with Iran, highlighted by President Barack Obama’s

landmark nuclear deal last year. The U.S. shale boom has also made

America far less reliant on Saudi oil.

“Buying bonds and all that

was a strategy to recycle petrodollars back into the U.S.,” said David

Ottaway, a Middle East fellow at the Woodrow Wilson International Center

in Washington. But politically, “it’s always been an ambiguous,

constrained relationship.”

Yet back in 1974, forging that

relationship (and the secrecy that it required) was a no-brainer,

according to Parsky, who is now chairman of Aurora Capital Group, a

private equity firm in Los Angeles. Many of America’s allies, including

the U.K. and Japan, were also deeply dependent on Saudi oil and quietly

vying to get the kingdom to reinvest money back into their own

economies.

“Everyone—in the U.S., France, Britain, Japan—was

trying to get their fingers in the Saudis’ pockets,” said Gordon S.

Brown, an economic officer with the State Department at the U.S. embassy

in Riyadh from 1976 to 1978.

For the Saudis, politics played a big role in their insistence that all Treasury investments remain anonymous.

Tensions

still flared 10 months after the Yom Kippur War, and throughout the

Arab world, there was plenty of animosity toward the U.S. for its

support of Israel. According to diplomatic cables, King Faisal’s biggest

fear was the perception Saudi oil money would, “directly or

indirectly,” end up in the hands of its biggest enemy in the form of

additional U.S. assistance.

Treasury officials solved the dilemma

by letting the Saudis in through the back door. In the first of many

special arrangements, the U.S. allowed Saudi Arabia to bypass the normal

competitive bidding process for buying Treasuries by creating

“add-ons.” Those sales, which were excluded from the official auction

totals, hid all traces of Saudi Arabia’s presence in the U.S. government

debt market.

“When I arrived at the embassy, I was told by people

there that this is Treasury’s business,” Brown said. “It was all

handled very privately.”

By 1977, Saudi Arabia had accumulated about 20 percent of all Treasuries held abroad, according to The Hidden Hand of American Hegemony: Petrodollar Recycling and International Markets by Columbia University’s David Spiro.

Another

exception was carved out for Saudi Arabia when the Treasury started

releasing monthly country-by-country breakdowns of U.S. debt ownership.

Instead of disclosing Saudi Arabia’s holdings, the Treasury grouped them

with 14 other nations, such as Kuwait, the United Arab Emirates and

Nigeria, under the generic heading “oil exporters”—a practice that

continued for 41 years.

The

system came with its share of headaches. After the Treasury’s add-on

facility was opened to other central banks, erratic and unpublicized

foreign demand threatened to push the U.S. over its debt limit on

several occasions. An

internal memo, dated October 1976, detailed how the U.S. inadvertently

raised far more than the $800 million it intended to borrow at auction.

At the time, two unidentified central banks used add-ons to buy an

additional $400 million of Treasuries each. In the end, one bank was

awarded its portion a day late to keep the U.S. from exceeding the

limit.

Most of these maneuvers and hiccups were swept under the

rug, and top Treasury officials went to great lengths to preserve the

status quo and protect their Middle East allies as scrutiny of America’s

biggest creditors increased.

Over the years, the Treasury

repeatedly turned to the International Investment and Trade in Services

Survey Act of 1976—which shields individuals in countries where

Treasuries are narrowly held—as its first line of defense.

The

strategy continued even after the Government Accountability Office, in a

1979 investigation, found “no statistical or legal basis” for the

blackout. The GAO didn’t have power to force the Treasury to turn over

the data, but it concluded the U.S. “made special commitments of

financial confidentiality to Saudi Arabia” and possibly other OPEC

nations.

Simon, who had by then returned to Wall Street,

acknowledged in congressional testimony that “regional reporting was the

only way in which Saudi Arabia would agree” to invest using the add-on

system.

“It was clear the Treasury people weren’t going to

cooperate at all,” said Stephen McSpadden, a former counsel to the

congressional subcommittee that pressed for the GAO inquiries. “I’d been

at the subcommittee for 17 years, and I’d never seen anything like

that.”

Today, Parsky says the secret arrangement with the Saudis

should have been dismantled years ago and was surprised the Treasury

kept it in place for so long. But even so, he has no regrets.

Doing the deal “was a positive for America.” —With assistance from Sangwon Yoon.

No comments:

Post a Comment